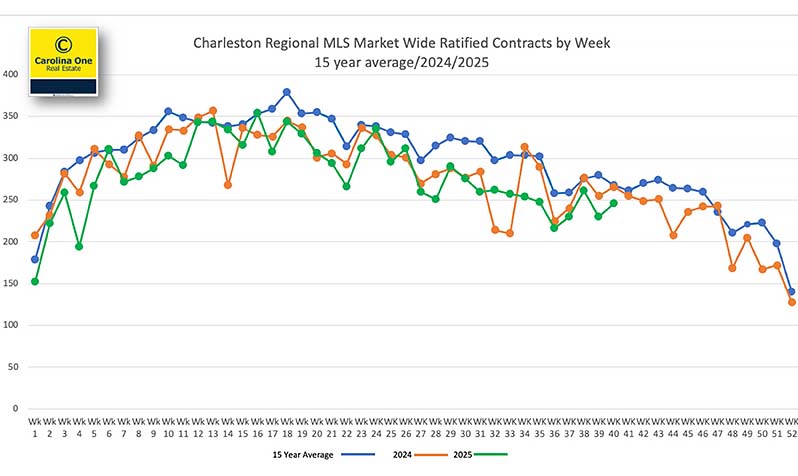

For the week of October 13 – 19, 2025) written sales jumped to 261 ratified contracts across the Charleston MLS – well above the ~200 and ~240 in the two prior weeks. August closed sales were essentially flat year over year (+1%), while August written sales finished a modest −2% versus August 2024. We’re easing into the normal fall slowdown, but opportunity remains abundant: with ~4,000+ sales still expected in 2025, there are thousands of chances to help clients make a move.